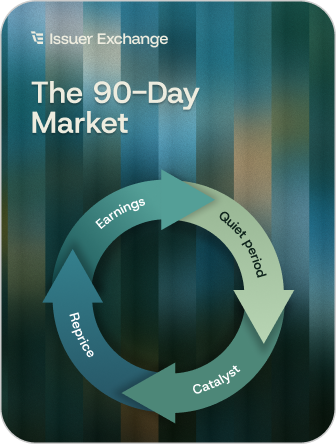

Public markets do not evaluate a company once and move on. They reassess continuously, but the quarterly cycle remains the core rhythm. Every 90 days, new evidence arrives. Expectations get compared with results. Shareholder confidence is either reinforced or weakened. The question is not whether the company will be judged inside that loop. It will. The real question is whether management is benefiting from that feedback cycle or paying for it.

Too often, issuers pay for it.

They pay through volatility that strips value from otherwise constructive progress. They pay through wider spreads that make ownership more fragile. They pay through churn that forces the company to reacquire attention over and over again. They pay through financings that happen on worse terms because the market has not been given enough reason to underwrite the story with confidence. Over time, these penalties add up. That is the dilution tax: the value lost when a company operates in the quarterly market cycle without enough intelligence, loyalty, or narrative discipline.

One public clean-technology company turned to Issuer Exchange after several quarters of fragile market response had already started to compound into a more expensive public-market position. The business had real merits and a credible long-term opportunity. Management was serious, the strategic thesis was understandable, and the company was progressing operationally. But the market experience remained frustrating. Good news did not hold as well as expected. Trading quality weakened between catalysts. Shareholder support felt thin and temporary. When capital planning entered the discussion, the company faced the risk that prior quarters of market fragility would now translate into a more expensive outcome.

Internally, management could point to progress. But the market had been repricing confidence every quarter, and the company had not built enough structure to benefit from that cycle. Each quarter’s uncertainty became the starting point for the next one. Instead of compounding trust, the company was compounding fragility.

After Issuer Exchange became involved, the company and its vendors began to treat the public market as an operating loop rather than a sequence of unrelated frustrations. Management paid closer attention to how the tape behaved after events, where shareholder churn was occurring, and which communications were actually creating more durable understanding. The company focused on building more repeat engagement, stronger event framing, and clearer continuity between updates. The goal was simple: turn the quarterly cycle from a tax into a flywheel.

That shift mattered because public markets can compound in either direction. When companies reduce uncertainty, improve liquidity quality, and strengthen the shareholder base, each quarter becomes a better foundation for the next. Trust leads to more stability. Stability supports better financing terms. Better terms preserve more control and help attract stronger holders. A stronger base, in turn, makes the next quarter easier to navigate.

So What Happened

Over time, the company’s market posture became less punitive and more constructive. Management had a clearer picture of what the stock was telling it, where trust was strengthening, and how to build on each quarter instead of resetting after it. The business itself had not been transformed overnight. What changed was the company’s ability to operate inside the rhythm of the public market.

Investor Feedback Capture

+58 pts

Investor feedback capture increased from 32% to 90% after the company began systematically recording investor questions, objections, concerns, and recurring points of confusion.

Message Adjustment Speed

+50%

Message adjustment speed improved by 50% as management identified recurring investor concerns faster and updated presentations, FAQs, and talking points before the next major outreach cycle.

Financing Readiness

+29 pts

Financing readiness improved from 44% to 73% after the company addressed investor concerns earlier, clarified its value proposition, and entered capital conversations with fewer unanswered questions.

This is where many issuers go wrong. They treat each difficult quarter as a separate problem rather than recognizing the pattern connecting them. But the market’s three-month compromise never ends. If management does not build intelligence and loyalty into that loop, value will continue to leak out through volatility, churn, spread weakness, and punitive financing.

The lesson is simple: you will either own the feedback loop or pay the dilution tax. Every 90 days, the market re-evaluates your company, your credibility, and your ability to convert progress into confidence. Issuer Exchange helps companies navigate that cycle with greater clarity, stronger shareholder engagement, and a more durable market strategy. Learn how Issuer Exchange can help you turn the quarterly loop into an advantage instead of a penalty.