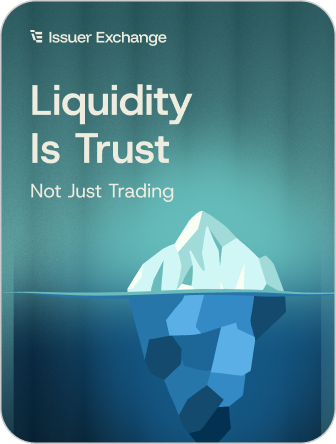

Liquidity is often described as a trading characteristic, something technical that sits outside management’s core responsibility. But for public companies, especially in the micro-cap and small-cap market, liquidity is not just a market detail. It is a visible confidence signal.

That is because liquidity affects how easily investors can move from interest to ownership. It shapes whether market makers feel comfortable narrowing spreads, whether institutions can realistically participate, and whether price discovery happens in a stable and credible way. In that sense, liquidity is not just about how much stock trades. It is about how much trust the market has in trading that stock.

When liquidity weakens, the warning signs are often easy to miss if management is not looking closely. Widening spreads signal that the market is charging a higher risk premium. Volume concentration around isolated events suggests fragile discovery rather than steady support. Off-exchange dominance can weaken visible price formation and make it harder for the public market to serve as a reliable mechanism for confidence. None of this is merely technical. It directly affects how the company is underwritten.

Before Issuer Exchange was brought in, one public manufacturing business had already begun to see weakening liquidity quality affect how the market was underwriting the stock. Management believed the company’s story was improving. Operational execution had become more disciplined, customer traction was building, and the business was beginning to show evidence that prior investments were starting to pay off. But the stock continued to trade with unusual fragility. Spreads remained wider than management expected. Volume clustered sharply around news, then disappeared. On quieter days, trading quality felt too thin to support confidence.

Internally, the company viewed this as frustrating but secondary. The assumption was that as the business improved, liquidity would improve on its own. But the market was already signaling something else. Investors were not simply reacting to the fundamentals. They were reacting to the friction around ownership itself. The stock was harder to trust as a vehicle, which meant even constructive operational progress was not translating as efficiently into confidence.

After engaging Issuer Exchange, the company and its vendors began to treat liquidity quality as a strategic indicator rather than a background condition. Instead of focusing only on price and daily volume, management looked more closely at spread behavior, average daily dollar volume, venue mix, and the durability of post-event participation. The company became more disciplined about how it framed announcements and how it interpreted the trading response afterward. The question was no longer just whether the market noticed the news. It was whether the news improved liquidity quality and visible market confidence.

That shift mattered. As the company aligned communications more tightly with investor-understandable milestones, it became easier to evaluate whether certain updates were helping the stock trade more credibly or simply creating short-lived activity. Liquidity was no longer treated as a passive feature of the ticker. It became part of the company’s feedback loop.

So What Happened

Over time, the company developed a clearer view of the difference between activity and trust. Management could see when participation was becoming more constructive and when fragility remained elevated. The stock did not suddenly become highly liquid overnight, but it became more understandable, and that improved how the company thought about future communication, investor engagement, and capital planning.

Average Daily Trading Volume

+39%

Average daily trading volume increased by 39% as investors gained more confidence in the company’s story, communication rhythm, and ability to explain progress between major announcements.

Investor Follow-Through Rate

+27 pts

Investor follow-through improved from 24% to 51% as more investors moved from initial interest to repeat engagement, meetings, watchlist activity, or active participation.

Bid-Ask Spread Efficiency

+17%

Bid-ask spread efficiency improved by 17% as the company’s clearer communications helped reduce uncertainty and improve investor familiarity with the stock.

This is where many issuers go wrong. They assume liquidity is something the market either gives them or withholds from them. But liquidity quality is often downstream of narrative clarity, shareholder composition, and how the market interprets risk. If management cannot see liquidity quality, it cannot manage the signals the market is already using to price confidence.

The lesson is simple: liquidity is trust, not just trading. Every quarter, the market reveals something about its confidence through how the stock actually trades. Issuer Exchange helps companies monitor that confidence more clearly so they can identify fragility earlier, strengthen the quality of the market around the stock, and make better decisions before liquidity weakness becomes a capital problem. Learn how Issuer Exchange can help you see and manage liquidity quality with greater precision.

Last Updated: 7 Jan, 2026