Public markets force tradeoffs on companies long before management feels fully ready to make them. The challenge is not just that compromise exists. It is that public companies are required to make important decisions in a live environment where the market reacts immediately, often before management has had a chance to frame the logic clearly.

This is where companies can get trapped.

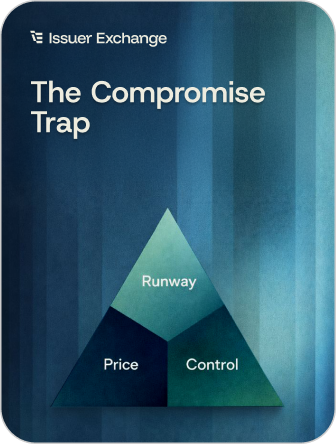

Every quarter presents some version of the same tension. Extend runway or protect the share price. Stay quiet until more is known or communicate early enough to reduce uncertainty. Preserve control or accept terms that may solve a near-term problem while creating a longer-term cost. These compromises are not unusual. They are part of being public. But for micro-cap and small-cap issuers, they often become more expensive than they need to be because they are made without enough visibility into how the tape will interpret them.

That is where many companies get trapped. Management may believe it is making the most rational choice available. Internally, the tradeoff may be obvious. But the market does not react to internal logic unless that logic is visible, measurable, and supported by a coherent pattern of execution. A financing that meaningfully extends runway can still be interpreted as distress. Silence intended to avoid overpromising can still create speculation. A decision that protects long-term value can still weaken confidence if shareholders are left to guess why it was necessary.

Before engaging Issuer Exchange, one recently listed industrial technology company was already struggling with a familiar public-market problem. The business had made real operating progress, but revenue conversion was taking longer than management had expected. The company still had strategic options, but it was approaching a window where additional capital might be needed to preserve flexibility. Internally, the team was weighing several compromises at once. Should it raise sooner and protect runway, even if the stock was not trading where management believed it should be? Should it wait for more operational proof points and risk shortening the timeline? Should it communicate more openly about the capital planning process or keep the market focused only on business execution?

The difficulty was not just the financing decision itself. It was that management lacked a clear picture of how the market was likely to absorb any of the available choices. The stock had shown occasional bursts of interest around updates, but those bursts had not translated into durable support. Volume appeared around announcements, then faded. Existing holders did not seem to be gaining conviction between quarters. The company was making a compromise either way. The question was whether it would make that compromise blind.

Once Issuer Exchange became involved, the company and its vendors began treating the problem as more than a capital question. It became a market-structure question. Instead of viewing the financing decision in isolation, management began to look at how liquidity quality, event response, and shareholder behavior were interacting. The company tightened the cadence of market communication, framed milestones more clearly, and focused on reducing the uncertainty that was causing the stock to trade below management’s own sense of intrinsic progress. This did not remove the need for compromise, but it changed the quality of the decision.

So What Happened

Over time, the company moved from reacting to pressure to managing tradeoffs with better visibility. Management gained a clearer sense of when the market was absorbing the story constructively and when fragility was increasing. The eventual capital strategy was approached with more context, stronger narrative discipline, and better alignment between what the company needed internally and what the market could reasonably underwrite externally. The compromise did not disappear. But it became more deliberate and less punitive.

Higher-Quality Investor Participation

+29 pts

Higher-quality investor participation increased from 34% to 63% after the company stopped chasing every source of capital and focused on investors aligned with its stage, strategy, and long-term value creation plan.

Discount Pressure Reduction

-22%

Financing discount pressure decreased by 22% as management entered capital conversations with stronger positioning, clearer market data, and less dependence on reactive financing options.

Shareholder Base Stability

+21 pts

Quarterly shareholder stability improved from 53% to 74% after the company became more selective about the investors it attracted and more disciplined in how it communicated the long-term opportunity.

This is where many issuers go wrong. They assume compromise is simply part of the job and that the market will eventually appreciate the logic. Usually it does not. Public markets punish uncertainty faster than they reward ambition. If management cannot clearly show how it is balancing runway, price, and control, the tape will assign its own interpretation, and that interpretation is often expensive.

The lesson is simple: every quarter forces a compromise, but blind compromise is what destroys value. The market is constantly reassessing how well management navigates tradeoffs under pressure. Issuer Exchange helps companies make those decisions with greater clarity, stronger shareholder engagement, and a more disciplined market strategy. Learn how Issuer Exchange can help you reduce uncertainty and make each quarterly tradeoff from a position of greater strength.

Last Updated: 7 Jan, 2026